Diversification means spreading your capital across assets whose performances are not perfectly correlated, in order to reduce overall risk without proportionally reducing expected return. It is often described as the only "free lunch" in finance: a reduction in risk that costs nothing in expected return. But diversifying well is more subtle than "buying lots of lines." This guide details the principles — correlation, position sizing, concentration, monitoring over time — to build a genuinely resilient portfolio.

Why does diversification reduce risk?

When two assets do not rise and fall at exactly the same time, their variations partially offset each other. The declines of one are cushioned by the stability or rise of the other. Mathematically, a portfolio's risk is not the average of its components' risks: it is lower as soon as the correlations are imperfect.

This is the heart of modern portfolio theory: for the same expected return, you can reduce volatility simply by combining assets that do not react the same way to the same events. Diversification does not remove market risk (the "systematic" risk that hits everyone), but it progressively eliminates the risk specific to each company.

What is correlation and why is it central?

Correlation measures how much two assets move together, on a scale from -1 to +1. A correlation of +1 means they move identically: holding them together provides no diversification. A low or negative correlation is what you are looking for.

A common trap: holding ten different technology stocks gives an impression of diversification, while their high correlation makes them fall together. The number of lines is reassuring, but it is the correlation between them that determines real protection.

Along which axes should you diversify?

Diversification is not limited to the number of stocks. It is built along several complementary axes: sectors (technology, healthcare, energy, finance…), geographies (United States, Europe, emerging markets), asset classes (equities, bonds, commodities, cash) and styles (growth vs value, large vs small caps).

The point is to choose axes that react differently to the same environment. For example, growth stocks and defensive stocks behave differently across the economic cycle; bonds often cushion equity shocks. Crossing these axes is more effective than stacking stocks of the same profile.

How many positions should you hold?

Research shows that most of the diversification benefit is reached with a reasonable number of well-chosen positions; beyond that, each additional line adds less and less. Too few positions expose you to high specific risk; an excessive number dilutes monitoring and brings the portfolio closer to a simple index, without its low fees.

The risk-reduction curve falls quickly then flattens: going from 1 to 10 lines hugely reduces specific risk; going from 30 to 50 adds almost nothing if the new lines are correlated with the old ones. The issue is therefore less the number than the low correlation between the lines — fifteen truly uncorrelated positions beat fifty variants of the same bet.

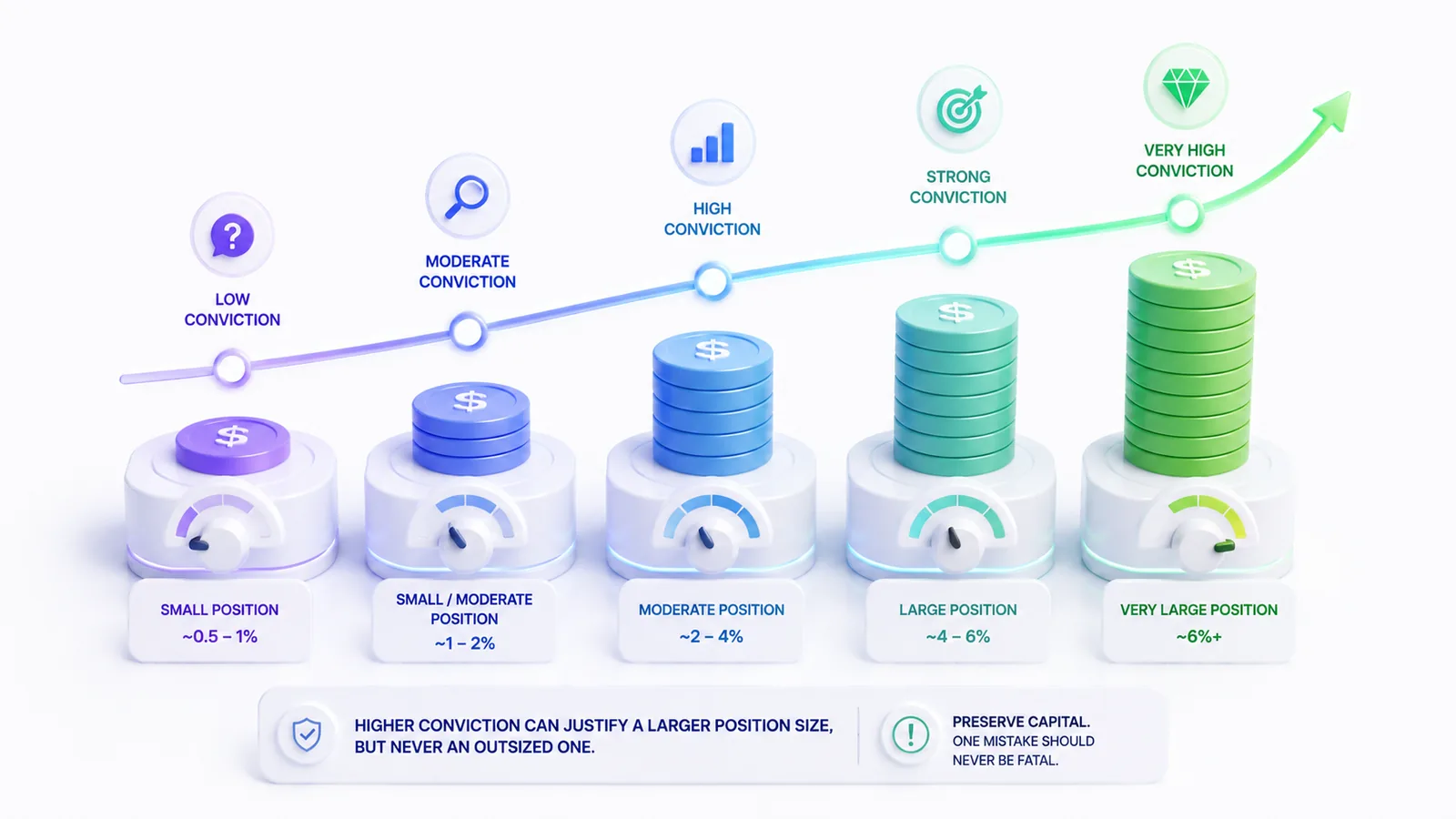

How to size a position?

A position's size should reflect the level of conviction and risk, not the enthusiasm of the moment. Approaches such as the Kelly criterion propose calibrating the size based on the probability of success and the expected gain/loss ratio. The practical rule: the stronger and the more confirmed the conviction across several signals, the larger the position can be, but never to the point of threatening the portfolio in case of error.

In practice, you often cap an individual line (for example at a few percent of the portfolio for a cautious investor) so that no single mistake is fatal. High conviction justifies a larger position, never an outsized one.

Concentration and specific risk

The opposite of diversification is concentration. It is measured by indices such as the HHI (Herfindahl-Hirschman Index): the more capital is concentrated in a few lines or a single sector, the more vulnerable the portfolio is to an isolated event.

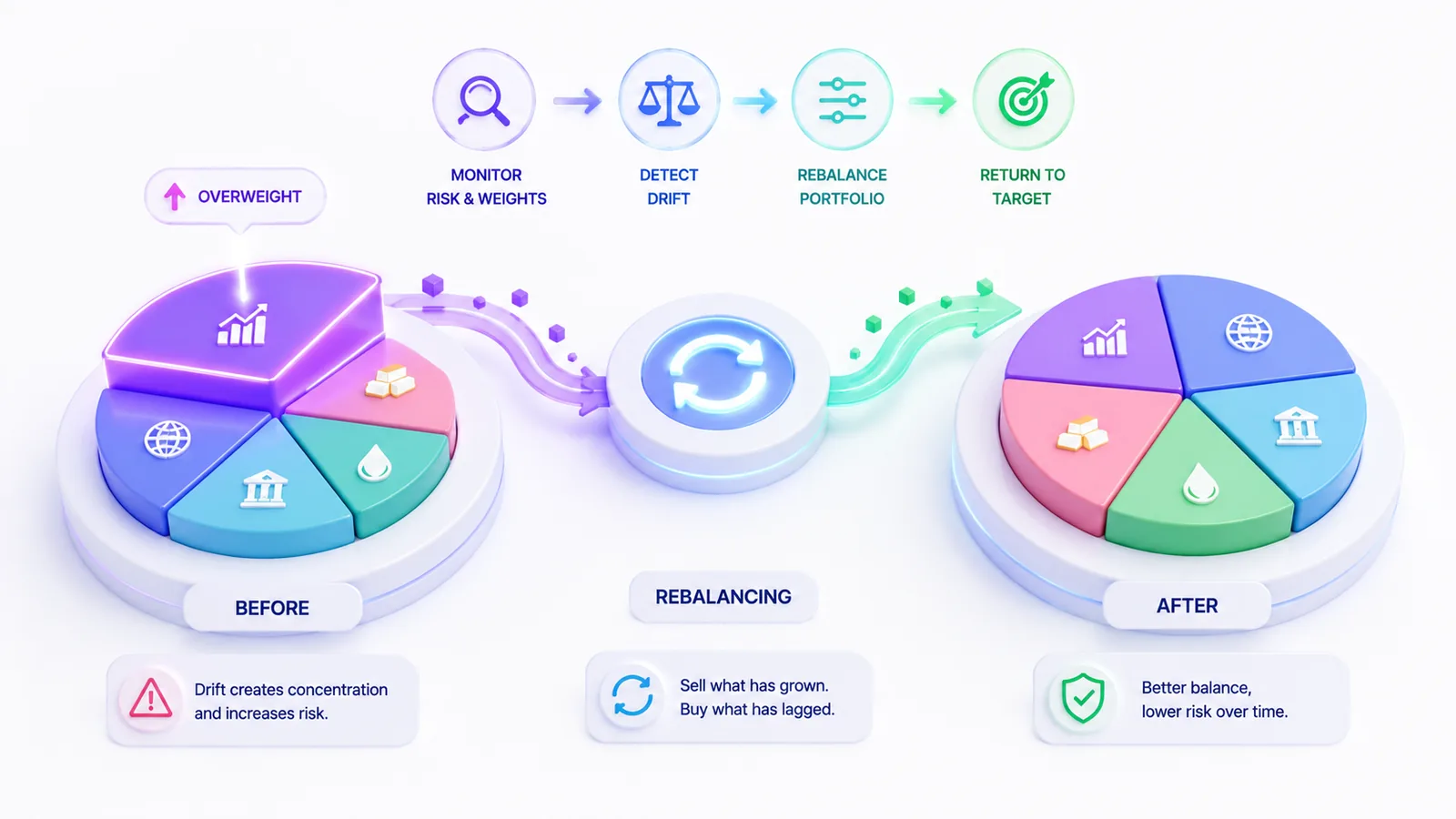

The most insidious danger is concentration that creeps in without a decision: a winning position that rises a lot eventually represents an outsized share of the portfolio. Success itself creates the risk. Monitoring the weight of each line and each sector is therefore a continuous discipline, not an initial setting.

How to monitor risk over time?

A well-built portfolio drifts over time. Rising positions take on growing weight, the allocation moves away from its target, and assets that were once uncorrelated can start moving together — that is the trap of stress periods, where correlations climb toward 1 and diversification protects least at the very moment you need it most.

Hence the importance of rebalancing: periodically bringing the allocation back toward its target by trimming what has grown too much. Monitoring concentration, correlation between lines and sector exposure is essential. InvestIQ applies this logic at the portfolio level with an aggregated health score and correlation alerts when two positions become too linked.

What mistakes should you avoid?

The classic pitfalls always recur: confusing the number of lines with real diversification; neglecting correlation and stacking stocks from the same sector; letting a winning position become disproportionate; underestimating the correlation that rises in a crash; and forgetting to rebalance. Risk management is not a one-off act but a continuous discipline, which often matters more than the search for the perfect stock.

Resilience before performance

Diversifying does not mean giving up performance: it means making sure you stay in the game long enough for performance to materialize. A resilient portfolio absorbs shocks without breaking, which lets you hold your winning positions over time. That is precisely what InvestIQ measures at the portfolio level — concentration, correlations, sector exposure — to turn a gut feeling about risk into a quantified monitor.

This is not investment advice.